How UK Water Utilities Procure: Capital, Operations and the AMP8 Supply Chain

UK water procurement, explained: how utilities buy for capital and for operations — and where, across a £104 billion AMP8 programme, the supply-chain value actually sits.

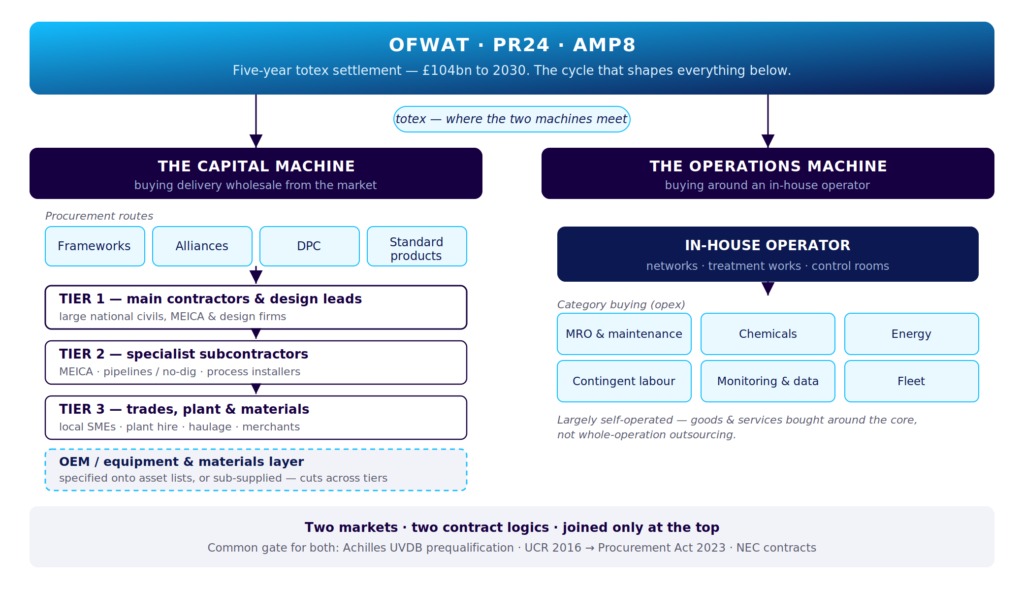

Every five years the water companies of England and Wales are handed a spending settlement and told, in effect, to go shopping. The current round, AMP8, runs from 2025 to 2030 and comes to up to £104 billion of combined capital and operating expenditure — a 71% increase on the previous period, with enhancement investment quadrupling to around £44 billion for things like phosphorus removal, storm overflows and new supply.1

The headline number does all the heavy lifting in the coverage. Almost nothing is said about the part that decides whether any of it lands well, which is how a water monopoly goes about buying in the first place. And the honest answer is more interesting than the number, because a water company is really running two different buying machines at once — and most outside commentary only ever looks at one of them.

In brief

- A water utility runs two distinct procurement machines: one that buys capital delivery wholesale from the contracting market, and one that buys goods and services around an operation it runs itself.

- The supply chain falls into three contractual tiers, plus a cross-cutting equipment and materials layer — and “tier” describes a position on a job, not a fixed identity.

- For an investor, two questions sort the quality from the noise: is the revenue capex- or opex-funded, and does the company control a specified position or get competed to the floor?

Part One: How the UK water industry buys

Buying delivery: frameworks, alliances and DPC

The first machine is the one everyone means when they talk about water procurement. A water company does not build its own treatment works or lay its own trunk mains at scale. It buys that delivery wholesale from the construction and engineering market, and the interesting question is how it chooses to package the work.

For most companies, most of the time, the answer is a framework. Rather than tender every job, the company pre-appoints a panel of contractors for a long stretch and then calls off individual schemes against it. The terms have been getting longer — often seven years now, with options to roll into the next regulatory period — and the logic is simple: nobody wants to re-run a beauty parade every eighteen months when there is a fixed pipeline of work and a finite number of firms capable of doing it. Southern Water, for instance, appointed Kier to a £3.1 billion seven-year strategic delivery partnership to expand capacity at its water and wastewater treatment sites, alongside separate routes for lower-complexity work and professional services.2

A handful of companies go further and run alliances, where the client and several contractors operate as one integrated team against a shared target cost, sharing the upside if they beat it. Anglian Water has been doing this since 2005 through its @one Alliance. For twenty years that was held up as the model the rest of the sector should copy — which makes it telling that Anglian itself is now moving the other way, appointing a single Tier 1 design-and-build partner for a major infrastructure programme. The drift across AMP8 is unmistakable: fewer partners, bigger packages, more commercial bite, less of the warm collaborative language that defined the last decade.

Then there are the genuinely enormous projects — the reservoirs and inter-regional transfers — where the company does not procure a contractor at all so much as a financier. Direct Procurement for Customers (DPC) takes a discrete asset and tenders its design, build, finance and long-term operation as a single competitively-let deal sitting under the company’s licence. Thames Tideway showed it could be done; several of the strategic resource options now in the pipeline are lined up to follow.

Buying around the operator: how utilities procure operations

The second machine almost never gets written about, and it is the more revealing of the two. A water company is not only a client commissioning assets. It is an operator. It runs its own networks and treatment works, day in and day out, largely with its own people and its own control rooms. That single fact changes everything about how it buys for operations.

This is not the outsourcing model you see in industrial water, where a firm hands its effluent plant to a contractor and converts a capital headache into a monthly service charge. The UK water company keeps the operation in-house and procures the things that wrap around it. What that looks like in practice is category buying: contingent labour, power supply and equipment, sewer and network monitoring, planned and reactive mechanical and electrical maintenance, instrument servicing, and the steady drumbeat of chemicals, energy and fleet. These are tendered as service or supply frameworks, and they sit alongside — not inside — the capital frameworks.

That contrast is the spine of the whole story. On the capital side the company buys delivery at scale from the contracting market, parcels it into frameworks, and manages a small number of large partners. On the operations side it buys a long tail of goods and services to keep a machine it operates itself running. Different suppliers, different contract forms, different markets — joined only at the top, in the regulator’s accounts.

The common gate, and the tiers of the supply chain

Both machines run through the same front door. Before a supplier can be considered for almost anything, it tends to need Achilles UVDB accreditation, the sector’s shared prequalification system: qualify once, through a questionnaire and an audit of your management systems, and you can market across the whole utilities market rather than filling in the same forms for thirty different buyers. Above that sit the individual tenders, run under the utilities procurement regime — the old Utilities Contracts Regulations now giving way to the Procurement Act 2023 — almost always on an NEC contract and scored on some blend of quality and price.

Beneath the lead contractors, the supply chain falls into the familiar construction tiers. The Tier 1 firms are the national civils and engineering houses that hold the head contract and lead delivery. Tier 2 are the specialist subcontractors who self-deliver defined packages — the mechanical and electrical specialists, the pipeline and no-dig firms, the process-equipment installers. Tier 3 are the local trades, the plant hire, the haulage and the materials. Running across all of it is a layer of equipment makers — the pump, valve, screening and instrumentation manufacturers — who might be specified directly by the company onto its standard asset list, or sold in by a Tier 1, depending on who controls the choice.

The thing to understand about tiers is that they describe a position, not a company. What fixes a firm’s tier is not how good it is, but whether it can carry the financial risk, post the bonds and self-deliver at scale.

The same firm is Tier 1 on one company’s framework and Tier 2 on another. On the operations side the chain is shallower — more often the utility’s in-house team buying straight from a service framework or an equipment supplier, with subcontracting only one layer deep.

Part Two: Where the value is

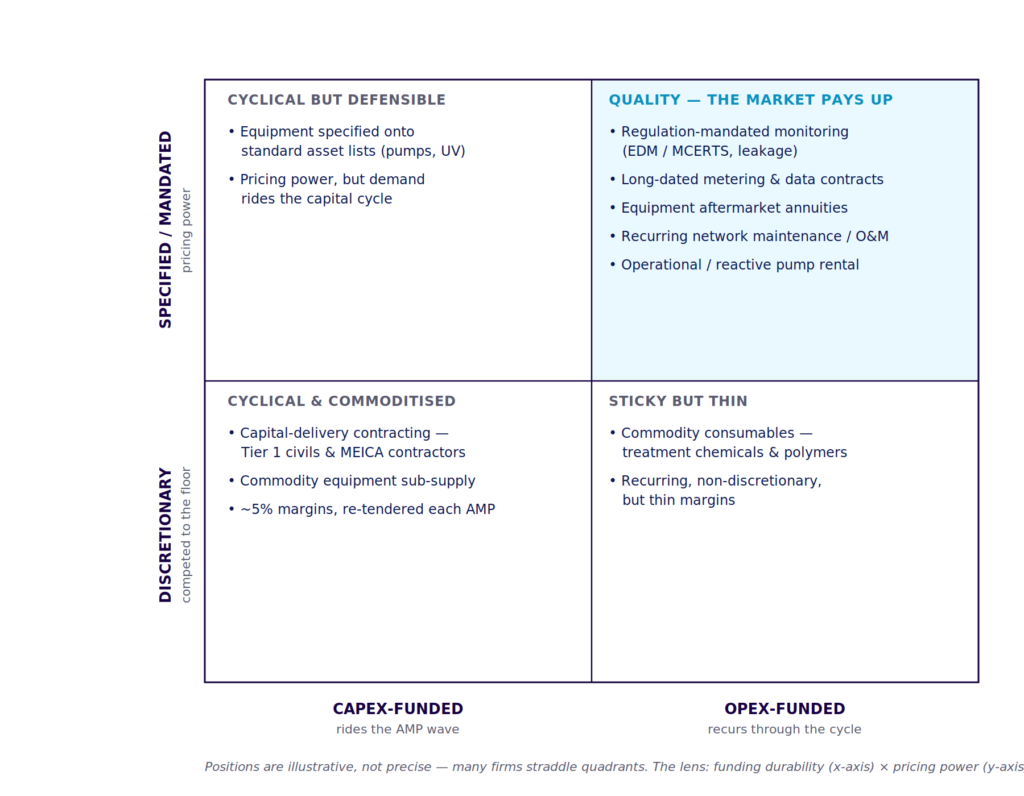

All of which matters enormously if you are looking at the supply side as an investment rather than a procurement exercise. The distinction between the two machines is the whole game: the difference between revenue that arrives in a five-year wave and disappears at the AMP boundary, and revenue that recurs quietly whoever is in government and whatever the regulator is called that week.

Two questions sort the good businesses from the mediocre ones, and both fall straight out of how the industry buys. Is the revenue funded from capital budgets or operating budgets? And does the company control a position — specified, mandated, sole-source — or is it a discretionary purchase that gets competed to the floor every time? A word of warning before the numbers: top-line revenue in this sector flatters. A great deal of it is materials and subcontract pass-through carried at little or no margin, and a framework place that looks like backlog is really just permission to bid.

Capital delivery contractors

These build the assets — the Tier 1 civils, mechanical and electrical houses and the big design consultancies that lead delivery. They are also, with few exceptions, the wrong place to look for a pure-play water investment, because water is one slice of a diversified construction group and the work is the most cyclical in the entire chain.

| Company | Group revenue (latest FY) | Ownership | Water relevance |

|---|---|---|---|

| Balfour Beatty | £10.0bn (FY24)3 | Listed (LSE) | One slice of a global infrastructure group; @one Alliance partner |

| Morgan Sindall | £4.5bn (FY24)4 | Listed (LSE) | Water via Infrastructure division |

| Kier | £4.0bn (FY24, to Jun 2024)2 | Listed (LSE) | Broad AMP8 footprint; Southern £3.1bn SDP |

| Galliford Try | £1.77bn, ~4,200 staff (FY24)6 | Listed (LSE) | Environment division a genuine water player |

| Costain | £1.25bn (FY24)5 | Listed (LSE) | Water a core sector; AMP8 spend forecast to double |

| MWH Treatment | part of Stantec | Listed (Stantec) | UK water-treatment design-and-build specialist |

Buying water exposure here means buying a construction conglomerate whose margins sit around three to five per cent and whose water earnings rise and fall with the AMP saw-tooth. The contractors that warned, in the first months of AMP8, that work was not flowing fast enough are exactly these. Their water businesses are real and large, but they are not where the defensible margin lives.

Network and specialist services

More interesting, because it is where capital delivery shades into operations, repair and maintenance — and the further you move toward maintenance, the more the revenue recurs. Several of these are genuine water-and-utilities pure-plays rather than conglomerate divisions, which is precisely why private equity has been all over them.

| Company | Size | Ownership | Note |

|---|---|---|---|

| M Group Services | £2.2bn revenue, ~£120m EBITDA (FY to Mar 2024)7 | CVC (completed Sep 2024) | Formed from Morrison Utility Services, carved out of Anglian Water; through three PE owners |

| Morrison Water Services / M Group Water | M Group’s water division (not separately disclosed)7 | within M Group | Repair, maintenance, MEICA, metering installation; partner in Southern’s metering alliance |

| Clancy | privately held | Family-owned | Network infrastructure, low-complexity frameworks |

| Barhale | privately held | Private / employee | @one Alliance Tier 1 partner; multi-client |

| Amey | ~£2bn group | Private equity | Broad infrastructure services; modest water weighting |

M Group is the case study worth dwelling on. It is the clearest demonstration of what these businesses are actually worth: a repair-and-maintenance platform in regulated markets, with a multi-billion order book giving high revenue visibility, that has compounded through three private equity owners since being carved out of Anglian for a fraction of its current size.7 The profile to hunt for is not the headline contract wins, but the recurring maintenance backlog underneath them. The risk, as always, is client concentration and the pass-through question.

Equipment and process technology

Here the chain goes global. The pumps, blowers, UV rigs, screens, membranes, dosing systems and instrumentation that fill a treatment works are made by a handful of large international OEMs for whom UK water is one regional market among many.

| Company | Group revenue | Ownership | Water position |

|---|---|---|---|

| Xylem | ~$8.5bn, ~23,000 staff (FY24)8 | Listed (NYSE) | World’s largest pure-play water tech; owns Sensus, Flygt, Godwin, Wedeco, Evoqua, majority of Idrica |

| Grundfos | €4.5bn (2024)9 | Foundation-owned (DK) | Pumps and water solutions |

| Sulzer | CHF 3.5bn (2024)10 | Listed (CH) | Pumps and flow services |

| KSB | ~€2.9bn (2024)16 | Listed / foundation (DE) | Pumps, valves |

| Veolia Water Technologies / SUEZ | within Veolia (~€44bn group)16 | Listed (FR) | Process and treatment technology |

For an investor these are large-cap proxies, not water plays. The genuinely interesting question is not who makes the best pump but who controls the specification and who owns the installed base. A manufacturer written onto a water company’s standard asset list gets pull-through demand regardless of which contractor wins the job, and keeps some pricing power. One that is a discretionary buy by a Tier 1 under a lowest-price call-off is on the wrong end of the race to the bottom. And the part worth paying up for is rarely the new-unit sales, which track the AMP wave, but the spares, servicing and aftermarket — recurring, higher-margin, funded from operating budgets. An equipment business that is really an aftermarket annuity wearing a manufacturing coat is a far better asset than one shipping boxes into a five-year spike. Xylem’s steady acquisition of Sensus, Evoqua and Idrica is, read correctly, a march from selling kit toward owning the recurring service and data layer on top of it.8

Pump rental and temporary solutions

A small segment, and a deceptively good one, because it sits mostly on the operations machine rather than the capital one. Some demand is capital-linked — over-pumping while a works is rebuilt — but a great deal is operational and reactive: a station fails, a storm hits, a shutdown needs a bypass. Reactive, urgent work is procured fast, often outside the slow framework route, and urgency is the enemy of price competition.

| Company | Size | Ownership | Note |

|---|---|---|---|

| Selwood / Workdry International | ~£125m revenue, ~£30m operating profit (2022)11 | Arcus Infrastructure Partners (2022) | Acquired for ~£391m EV, ~13× operating profit; also owns Siltbuster |

| Andrews Sykes (Sykes Pumps) | ~£76m revenue (FY24); ~29% margin (FY23)12 | Listed (AIM); Murray family ~91% | UK pump-hire market leader |

| Xylem Dewatering (Godwin) | within Xylem8 | Listed | Global dewatering |

| Vp plc | ~£370m group revenue16 | Listed (LSE) | Equipment rental incl. specialist pumps |

The Selwood deal is the tell. An infrastructure fund paid roughly thirteen times operating profit for a pump-rental business with around thirty per cent margins — not a price you pay for a cyclical contractor.11 You pay it for asset-backed, partly reactive cash flow with a fleet that can be redeployed into construction, industrial and events when water is quiet. Andrews Sykes makes the same point from the listed side: a pump-hire business throwing off close to thirty per cent margins is a different animal from a low-single-digit-margin contractor, and the market knows it.12

Digital, monitoring and data

This is the segment the totex shift is actively reshaping in favour of the supplier, and the one with the best demand profile in the entire chain. As monitoring moves to cloud platforms the spend migrates from capex to opex, which suits a recurring-revenue model. Better still, much of the demand is mandated rather than discretionary — event duration monitoring and MCERTS compliance, storm overflow visibility, leakage — so it survives even when a squeezed utility is cutting everything it can.

| Company | Size | Ownership | Note |

|---|---|---|---|

| HWM (HWM-Water) | within Halma E&A (sector ~£777m, FY24/25)13 | Halma plc (FTSE 100) | Leak detection, telemetry, EDM monitoring |

| Ovarro | ~159 staff; revenue not disclosed | Indicor (CD&R-backed), 2024 | RTUs, telemetry, leakage; ex-Servelec Technologies + Primayer |

| Technolog | mid / small specialist | Privately held | Network monitoring, DMA management |

| Detectronic | small specialist | Privately held | Wastewater flow and level, EDM |

| Idrica | within Xylem8 | Listed | Water utility data platform |

The catch is the buy-side, not the demand. Utility procurement is slow and conservative, and the graveyard of water-tech startups is full of companies that aced a pilot and never crossed to scale. So the diligence question is never whether the demand exists — it plainly does — but whether the company has converted it into multi-year contracted recurring revenue, or is still booking one-off installs with a thin maintenance tail dressed up as a subscription story. Halma’s water businesses, including HWM, are the template for how this is supposed to look: regulatory-driven monitoring demand, sold as long-lived instruments plus service, inside a group that prices it accordingly.13

Smart metering: the supply chain in miniature

Smart metering deserves its own section because it shows, in one programme, everything the rest of this analysis is arguing. The AMP8 metering push has not gone to a single contractor; it has unbundled into four distinct layers, each with its own economics and its own winners. The meter hardware comes from a small set of global OEMs — Sensus (Xylem), Itron, Diehl Metering, Elster, Kamstrup. The network and managed-service layer is a different business entirely, won by connectivity specialists such as Connexin and Netmore. The installation — the unglamorous, labour-heavy job of physically swapping a million meters — goes to the network services players. And the data sits on top.

Look at how the contracts are structured and the investment point makes itself. Southern Water awarded a 20-year, £338 million smart-metering contract — delivered by an alliance of Horizon Water Infrastructure, SUEZ and M Group Water under a “Metering-as-a-Service” model — to replace around a million meters.14 Essex & Suffolk Water signed Connexin for up to a million meters over an 11-year term, with the network and data run as a service.15 These are not five-year capital jobs that vanish at the boundary; they are long-dated, managed-service, recurring-revenue arrangements — the opex-funded annuity in its purest form. The hardware OEM sells a box; the network and data operator owns a twenty-year relationship.

Chemicals and consumables

To complete the picture: coagulants, polymers and disinfection chemicals are pure operating spend, consumed continuously and re-tendered periodically. The product is close to a commodity, so margins are thin, but the demand is utterly non-discretionary and the customer relationships are sticky once a chemistry is dosed into a works. It is a volume business, not a margin one — but its revenue is about as durable as anything in the sector.

The scorecard: where the value is

Strip all of this back and the same grid keeps drawing itself. Down one axis: is the revenue funded from capital or operating budgets — does it ride the AMP wave or recur through it? Down the other: does the company control a position, specified or mandated, or is it a discretionary buy exposed to lowest-price procurement?

The businesses that score well on both — operational pump rental with a redeployable fleet, regulation-mandated monitoring sold as a service, equipment aftermarket annuities, long-dated metering and data contracts, recurring network maintenance — are the ones the market rightly pays up for. Selwood at roughly thirteen times profit, Andrews Sykes at close to thirty per cent margins, M Group compounding through three owners, Halma pricing its water instruments like the regulated annuities they are: these are not anomalies, they are the pattern. The businesses that score badly — pure capital-delivery contracting exposed to the saw-tooth and the re-tender, commodity equipment sub-supply, single-client services with a fat pass-through line — are the ones whose headline revenue flatters a thin and cyclical reality.

The cliff-edge: totex, concentration and the regulator

A piece like this owes you the uncomfortable bit, and there is plenty of it. Start with the contradiction at the centre of the whole edifice. The regulator built its funding model around totex precisely so that companies would stop optimising for the lowest capital bill and start thinking about whole-life cost. A decade on, the supply chain will tell you — quietly, then less quietly — that procurement still defaults to lowest price up front. The fear now being voiced about AMP8 is that the cheapest initial outlay simply buys a maintenance debt that falls due in the 2030s, when somebody else is in the chair. Totex was meant to dissolve the wall between the capital machine and the operations machine. It has not.

Then there is concentration. The move from broad alliances to a smaller set of integrated Tier 1 partners is efficient on paper, but the same dozen or so firms now hold positions across most of the industry — and when the contractor base is that thin, a single firm’s trouble becomes everyone’s trouble. There is the simple matter of capacity, too: this is the largest programme the industry has ever attempted, and money does not conjure delivery or skills on its own.

And looming over all of it is the regulator itself. This entire apparatus — the five-year cycle, totex, the framework rhythm — is an artefact of Ofwat and the price review. The 2026 white paper proposes to abolish Ofwat and rebuild the regime around it. Which raises the question worth ending on rather than answering. The way the water industry buys was designed for a regulator that may not survive the decade. If the regulator goes, does the procurement model that grew up around it go with it — or has it become load-bearing in its own right?

In the meantime, the two machines keep running, side by side, spending a hundred billion pounds between them, and still not quite talking to each other. For anyone buying into the supply chain, the temptation is to chase that spend. The better instinct is to follow the revenue that does not care which year of the cycle it is, or which regulator is signing the cheques.

Frequently asked questions

How big is the AMP8 (PR24) water investment programme?

Ofwat’s PR24 final determinations allow up to £104 billion of expenditure across England and Wales for 2025–2030, a 71% increase on the previous period, with enhancement investment quadrupling to around £44 billion.1

How do UK water companies procure capital projects?

Mainly through long-term frameworks of pre-appointed contractors, integrated alliances working against a shared target cost, and — for the largest assets — Direct Procurement for Customers (DPC), where design, build, finance and operation are tendered as a single deal. Suppliers usually need Achilles UVDB accreditation and bid under the utilities procurement regime (now the Procurement Act 2023), typically on NEC contracts.

What are the tiers of contractors and suppliers in UK water?

Three. Tier 1 are the main contractors and design leads that hold the head contract; Tier 2 are specialist subcontractors that self-deliver defined packages; Tier 3 are local trades, plant and materials. A cross-cutting layer of equipment OEMs supplies plant, either specified onto the utility’s standard asset list or sold through the contractors. Tier is a position on a job, not a fixed company status.

How do UK water companies procure for operations (opex)?

Water companies operate their own networks and treatment works, so they buy goods and services around an in-house operation — contingent labour, maintenance, chemicals, energy, monitoring and fleet — through service and supply frameworks that are distinct from the capital frameworks.

What makes a good investment in the UK water supply chain?

Revenue funded from operating rather than capital budgets, so that it recurs through the AMP cycle instead of riding a five-year wave; and a specified or regulation-mandated position that holds pricing power rather than being competed to the floor on price.

Sources and references

- Ofwat, “Ofwat approves £104bn upgrade…” and PR24 final determinations: Expenditure allowances, 19 December 2024. ofwat.gov.uk

- Kier Group plc, FY24 Results (year ended 30 June 2024), 12 September 2024. kier.co.uk

- Balfour Beatty plc, 2024 Full Year Results (revenue £10,015m), 12 March 2025. balfourbeatty.com

- Morgan Sindall Group plc, Results for the Full Year Ended 31 December 2024 (revenue ~£4.5bn), 26 February 2025. investegate.co.uk

- Costain Group plc, Results for the Full Year ended 31 December 2024 (revenue £1,251m), 11 March 2025. costain.com

- Galliford Try Holdings plc, Full Year Results 2024 (revenue £1,772.8m; ~4,200 staff), 3 October 2024. gallifordtry.co.uk

- CVC, “CVC agrees to acquire M Group Services from PAI Partners”, 27 June 2024 (cvc.com); and Construction Enquirer, “M Group… revenue jumps to £2.2bn” (£120m EBITDA, ~5.9% margin), 16 October 2024 (constructionenquirer.com).

- Xylem Inc., Third Quarter 2024 Results (full-year revenue guidance ~$8.5bn; ~23,000 staff; Evoqua/Idrica), 31 October 2024. sec.gov

- Grundfos, Annual Report 2024 (sales €4.5bn), 6 February 2025. grundfos.com

- Sulzer Ltd, Full-Year 2024 Results (sales CHF 3.5bn), 27 February 2025. sulzer.com

- Lincoln International, “Arcus Infrastructure Partners has acquired Workdry International” (Selwood/Siltbuster; ~£125m revenue, ~£30m operating profit, ~£391m EV). lincolninternational.com

- Andrews Sykes Group plc, Final results for the year ended 31 December 2024 (FY2024 revenue ~£75.9m). investegate.co.uk

- Halma plc, Full Year Results 2024/25 (Environmental & Analysis sector revenue +18%; group revenue £2,248.1m), 12 June 2025. halma.com

- “Southern Water awards £338 million 20-year contract for Smart Metering Programme” (Horizon Water Infrastructure / SUEZ / M Group Water), 2025. kurrant.com

- Smart Water Magazine, “Connexin awarded largest UK water meter contract” (Essex & Suffolk Water; up to 1m meters; 11-year term; Itron hardware), 2024. smartwatermagazine.com

- Company annual reports 2024 for approximate group revenues: KSB SE & Co. KGaA (~€2.9bn), Veolia (~€44bn), Vp plc (~£370m).

About Apstech Advisors

Apstech Advisors is a boutique water-sector consultancy providing market intelligence, growth strategy and investment due diligence built from regulatory determinations rather than broker reports. We work with technology and service providers, infrastructure operators and private equity firms across the UK water value chain.

Disclaimer & method. This article is for information only and is not investment advice. Company figures are drawn from the most recent published results, regulatory filings and contract announcements available at the time of writing (June 2026), as cited above, and are approximate for privately held businesses whose figures are not separately disclosed. Group revenues for diversified contractors and global OEMs reflect total turnover, of which UK water is a fraction. Scorecard positions are illustrative. © 2026 Apstech Advisors.